Amidst the hustle and bustle and tranquility of Mumbai’s financial district, 53-year-old Dr. Rahul Gupta stands at a new starting point in his career. This experienced investment expert, who worked at Fidelity Investments in the United States for nearly 20 years, sees his return to India from the US in 2025 not simply as a homecoming, but as the beginning of a long-planned “financial mission.”

Capital accumulation across mountains and seas

Dr. Rahul Gupta’s twenty years at Fidelity Investments were the most significant chapter of his career. As a top global asset management firm, Fidelity is renowned for its rigorous investment philosophy and exceptional risk management system. There, Rahul not only witnessed firsthand the ups and downs of the global financial markets but also accumulated extensive practical experience in asset allocation, risk control, and cross-market research.

He personally witnessed the information gap between ordinary investors and professional institutions and deeply understood the profound impact of “financial literacy” on personal wealth growth and even national economic vitality. With this impressive resume and boundless aspirations for the potential of the Indian market, Rahul returned to his long-lost hometown of Mumbai in mid-2025.

Establishing the “Financial Literacy Enhancement Academy”: From knowledge transfer to practical skills development

Upon returning to India, Dr. Rahul Gupta spent over six months conducting in-depth research. He astutely observed that with India’s booming economy, both young professionals just entering the workforce and high-net-worth individuals with substantial wealth faced a common pain point: a lack of systematic financial education and the difficulty in translating knowledge into practical investment skills.

To break this deadlock, Rahul decided to launch the Financial Literacy Enhancement Academy. This is not just a school, but an incubator aimed at cultivating high-caliber financial professionals with capabilities in financial market analysis, investment decision-making, risk control, and wealth management.

Unlike traditional educational training institutions, the academy adopts a teaching system framework of “theory + practice + long-term growth,” constructing a complete growth path from “basic understanding – framework building – practical application.”

• Foundational Understanding Stage: Helps students systematically master basic financial market knowledge, macroeconomic analysis, corporate fundamentals research, and common financial instruments.

• Framework Building Stage: Focuses on cultivating logical thinking, data-driven decision-making, risk control systems, and long-term value investing principles, emphasizing independent thinking, discipline, and “second-level thinking” to avoid blindly following trends and short-term speculation.

• Practical Application Stage: Through real stock investment simulations and case studies, students, under the guidance of mentors, directly apply the learned methods to the market environment, gradually forming their own investment system.

Dr. Rahul Gupta will personally provide detailed instruction in the group, offering personalized support to learners at different levels, including investment beginners, professionals, corporate executives, and high-net-worth investors.

Addressing Concerns: Be Vigilant Against Financial Fraud and Safeguard Rational Learning

In recent years, the Indian financial education sector has indeed seen some unscrupulous institutions using the lure of “high returns” and “quick riches” to commit fraud. These include promises of guaranteed high returns, fundraising schemes, and various fraudulent transactions involving foreign exchange and cryptocurrencies, as well as “training traps” that demand large upfront fees without providing any substantial course content. These issues have made many potential investors hesitant.

Financial Literacy Enhancement Academy proactively addresses this reality. The academy’s core focus is on knowledge transfer and skills development, not fundraising. All course content revolves around rigorous risk control and long-term value investing, helping students develop sound financial literacy and avoid various financial scams.

Outlook: A co-creation platform for future investors

From a senior expert at Fidelity Investments to a pioneer in financial literacy education in India, Dr. Rahul Gupta has used his two decades of professional experience to build a bridge connecting ordinary people with professional investment.

Here, there are no theoretical exercises, only systematic methods and practical drills; no one-way knowledge transfer, only mentorship based on trust and student growth.

For Dr. Rahul Gupta, the establishment of the Financial Literacy Enhancement Academy is not only about sharing the valuable experience of top international investment banks, but also about pioneering a rational and transparent path in Indian investment education. As he says, “What we are doing is not an ordinary academy, but a co-creation platform to help Indian investors achieve long-term, stable growth.”

If you also aspire to bridge the gap between “retail investor thinking” and “professional thinking,” welcome to join the Financial Literacy Enhancement Academy, where we can use the right knowledge and rigorous methods to protect our wealth and illuminate our future.

Daily writing prompt

How have you adapted to the changes brought on by the Covid-19 pandemic?

Faceless assessment represents a watershed shift in Indian tax administration — from traditional, physical, and often discretionary tax officer interactions to a digitized, transparent, and process-driven system. Initiated under the Income-tax Act, 1961, this reform has sought to eliminate geographical jurisdiction, reduce taxpayer harassment, and infuse accountability into the tax assessment process. With the Government of India introducing the Income Tax Act, 2025 to replace the nearly six-decade-old 1961 Act from 1 April 2026, significant structural and procedural changes have been proposed in the assessment regime, including refinements to faceless assessments.

This article provides a comprehensive analysis of the Faceless Assessment Scheme, tracing its legislative evolution, institutional architecture, procedural mechanics, and technological backbone. It examines the scheme’s legal foundation under Section 144B of the Income Tax Act, 1961, and its proposed continuation under Section 273 of the incoming Income Tax Act, 2025. Drawing on judicial pronouncements, academic insights, and stakeholder feedback, the article critically evaluates the operational challenges such as procedural delays, over-engineering of units, and the dilution of natural justice that threaten to undermine the scheme’s original vision.

Further This article highlights the transformative potential of faceless assessment in improving efficiency, and fostering taxpayer trust. It concludes with actionable policy recommendations advocating for structural simplification specifically, the abolition of redundant Technical and Review Units to restore accountability, improve assessment quality, and ensure that the faceless regime fulfils its promise of a fair, efficient, and justice-oriented tax administration.

Keywords: Faceless Assessment, Income Tax Act 1961 (Section 144B), Income Tax Act 2025, Section 273, Section 532, NeAC, Tax Transparency, Digital Governance, CBDT, Tax Reform, Finance Budget.

Introduction: Tax Law and Administrative Reform in India

India’s taxation system has evolved over decades, anchored for the last sixty years in the Income-tax Act, 1961. Despite periodic amendments aimed at modernizing the system, the legacy Act accumulated complex language, procedural inefficiencies, and litigation challenges. Recognizing the need for a revamped statutory framework, the legislature introduced the Income Tax Bill, 2025, designed to replace the older law with a streamlined, modern, and digitally oriented statute. Among its key reforms is the embrace and enhancement of the faceless tax regime, a flagship reform initiated under the 1961 Act but carried forward and embedded within the 2025 Act’s procedural architecture.Faceless assessment seeks to augment transparency, reduce human discretion, and leverage technology for efficient tax administration. This article analyses the current law’s faceless assessment regime and juxtaposes it with the approach under the new statutory framework.

Background: The Concept of Faceless Assessment

Stakeholders widely agreed that India’s income tax system was once crippled by a rigid, location-based structure, which bred chronic inefficiency, a profound lack of transparency and entrenched unfair practices. The reliance on face-to-face dealings between taxpayers and tax officers often gave rise to prolonged delays and subjective bias.In the annual conclave of Tax Administration Authorities, “RajaswaGyanSangam”, held in June 2016, Honourable Prime Minister Shri Narendra Modi Ji advocated tax administration reforms through the ‘RAPID’ approach standing for Revenue, Accountability, Probity, Information, and digitization. To transform age-old manual assessment methods, enhance transparency, efficiency, and accountability, and curb malpracticesthe E-Assessment Scheme 2019 was launched on 7 October 2019. The Finance Ministry launched the “Transparent Taxation – Honouring the Honest” platform on August 13, 2020, to ease taxpayers’ burdens and rebuild their trust in India’s tax system. This initiative rests on three key pillars: Faceless Assessment, Faceless Appeal, and the Taxpayers’ Charter. The heart of this reform lies the Faceless Assessment Scheme (FAS). It replaces from a system where tax assessments were conducted by a known officer in a known jurisdiction to one where both the assessing authority and the taxpayer remain anonymous throughout the process. The scheme was conceived not merely as a procedural upgrade but as a cultural and institutional transformation that rebuilds trust between the government and honest taxpayers

What is Faceless Assessment Scheme (FAS)?

Faceless assessment marks a significant evolution in India’s income tax administration, where the complete evaluation of a taxpayer’s income tax return occurs electronically, without any physical interaction or personal interface between the assessee and tax officials. Launched via the Faceless Assessment Scheme (FAS) in 2020 and integrated into the Income Tax Act, 1961 (as amended), this system aims to minimize discretionary authority of assessing officers, remove territorial jurisdiction limitations, and prevent instances of harassment or undue interference.

The process powered by the use of sophisticated advanced digital platforms, primarily the Income Tax e-filing portal (incometax.gov.in), which facilitates seamless operations. These include automated generation and issuance of notices under sections such as 143(2) or 142(1), secure online uploading of documents and responses by taxpayers, prompt handling of queries or show-cause notices, and electronic delivery of final assessment orders. Officers, based at faceless National e-Assessment Centres (NeACs) and Regional Faceless Centres (RfCs), are assigned cases randomly through algorithmic selection to uphold uniformity and objectivity. This shifts their role from traditional territorial adjudicators to streamlined, technology-enabled processors emphasizing data analysis and regulatory adherence.The rationale and Objectives for faceless assessment Scheme includesAll digital interactions are logged and traceable, reducing scope for arbitrary actions.Centralized processing and AI-assisted case allocation expedite handling which may reduce jurisdictional Bias and enhanced taxpayers experience.

Faceless Assessment under the Income-tax Act, 1961:

Statutory Legal Basis: Under the Income-tax Act, 1961, faceless assessment was introduced through Section 144B, empowering the Central Board of Direct Taxes (CBDT) to define the faceless assessment process and procedures. The Central Board of Direct Taxes (CBDT) operationalized the scheme through Notification No. 60/2020 dated 13th August 2020, which laid down the procedural and structural framework for faceless assessments. This notification along with subsequent amendments, established the institutional architecture, communication protocols, and operational guidelines. The provision mandated digital issuance of notices and electronic submissions of responses, including through video conferencing when needed. The key components in Faceless Assessment scheme includes:

Electronic Notices: Initiation of assessment by the officers should be by issuing digitally served notices.

Digital Responses: Taxpayers must furnish responses and documents through the Income Tax e-filing portal.

Random Allocation: The system automatically allocates assessment cases to assessing officers outside territorial jurisdictions except the cases of Search and survey.

Video Conferencing:Wherever Taxpayers feel that he wishes to explain the things orally as it is difficult to explain on paper he may seek personal hearings online through video conferencing if necessary. In this process also identity of the officer is not disclosed.

Audit Trail: Comprehensive logging ensures accountability and traceability.

Operational Workflow

The faceless assessment workflow under the 1961 Act generally involved:

Notice Issuance: The e-filing system issues assessment notices (e.g., under Sections 142(1), 143(2), or 148 etc.).

Document Submission:After receipt of the notice taxpayers upload his submission along with supporting documents and respond to queries online.

Assessment Draft order:Assessing officer prepare draft assessment order based on various submission made by the taxpayers and data collected by him by issuing notice U/s. 133(6) of the Income Tax Act 1961.

Submission against Draft order: Taxpayers can either object the draft order or accept the order after verification of the draft order.

Video Conferencing: Assessee can opt for the Video conferencing for argue the case orally.

Revised or Final order: After verification of submission to draft order Assessing officer prepare final order and send it for approval.

Quality Review: Independent review panels ensure quality and fairness of the order.

Final Assessment Order:After all this process the final Assessment order is issued electronically in compliance with statutory timelines.

Limitations and Challenges of the 1961 Faceless Assessment Scheme:

While faceless assessment marked a significant improvement, several limitations under the 1961 Act emerged. Major limitations are:

Technological Adaptation: Older provisions were adapted to digital procedures but not inherently drafted for modern technology.

Procedural Complexity: Notices and responses under the 1961 Act require interpretation of multiple sections and cross references which could complicate digital automation.

Limitation of Space and size for document upload: The submission and relevant document uploaded through income tax portal is having limited space. At a time only 10 attachments can be upload and single attachment should not be more than 5 MB in size. It creates difficulty to taxpayers while submitting the submission.

Limited Scope for Clarification: Some taxpayers faced delays when seeking online hearings or clarifications.

Litigation Bottlenecks: Despite digital procedures, disputes continued due to ambiguities in language and procedural overlaps.

These concerns set the stage for a reimagined legislative approach under the Income Tax Act, 2025, which aims to build a more coherent digital assessment framework.

Overview of the Income Tax Act, 2025

The Income Tax Act, 2025 represents a comprehensive overhaul, replacing the fragmented 1961 law. It aims to achieve simplicity, efficiency, and taxpayer clarity. Key features include:

Reduced Length and Complexity: Sections are reduced from over 800 in the 1961 Act to 536, and the overall legislative language is simplified.

Unified Tax Year Concept: The traditional previous year and assessment year are eliminated, replaced by a single tax year concept.

Digitization Emphasis: Enhanced digital compliance tools, including faceless assessments and digital notice systems.

Importantly, the new Act will come into force on 1 April 2026, with new Income Tax Return (ITR) forms and rules notified prior to implementation. New Income tax rules are yet to be notified.

Faceless Assessment under the Income Tax Act, 2025:

Codification and Redrafting:Under the Income Tax Act 2025, provisions related to faceless assessment have been redrafted and consolidated to align with the overall objectives of clarity and digital orientation:

Consolidation: The old Section 144B of the 1961 Act, which detailed faceless assessment procedures, is re-drafted as Section 273 (or equivalent) in the new Act, ensuring a cohesive approach that is integrated with other digital compliance mechanisms.

Scheme Power: Section 532 empowers the Central Government to frame faceless schemes eliminating interface with taxpayers, a structural enhancement reinforcing the digital approach across procedures.

Procedure Clarity: Notices, responses, and procedural steps are consolidated and clarified, aiming to reduce ambiguity and streamline compliance.

Key Changes and Enhancements:

The new Income Tax Act 2025 approach includes Broader Digital Integration. Faceless assessments are deeply integrated with the Act’s digital infrastructure. Enhanced tools includethe statutory design envisions algorithmic distribution of cases to reduce bias and improve turnaround, Digital service of notices and assessment outcomes remain core components and use of Artificial intelligence for assessment procedure.These reinforce the objective of zero physical interface between the taxpayer and tax officials. The new Act expands what constitutes information for the purpose of issuing notices including directions from approving panels and findings from judicial or tribunal orders. This is procedural but critical in digital notice scenarios.

Procedural Simplification

By removing redundant procedural provisions and presenting faceless assessment provisions in a consolidated format.The Income Tax Act 2025 Act aims to Reduce confusion arising from historical cross-referencing of multiple sections, simplify notice issuance requirements and timelines and importantly harmonize digital process steps across assessment, reassessment, and appeals.

Comparative Analysis: Faceless Assessment in 1961 vs 2025 Act:

The transition from the Income-tax Act, 1961, to the Income Tax Act, 2025, blends continuity with significant transformation across key aspects of tax administration. Under the 1961 Act, the statutory base for faceless assessments relied on Section 144B, which tied provisions to the Act’s procedural context, whereas the 2025 Act integrates these into a native digital procedural architecture with consolidated provisions under newer sections and scheme-making powers.

The digital interface evolved from gradual adaptations of existing e-filing systems in the 1961 framework to a fully cohesive, native digital orientation in 2025, supported by streamlined statutory rules. Procedural complexity decreases notably in the new Act, moving away from the legacy language and cross-references of 1961 toward simplified phrasing, consolidated steps, and table-based presentations for greater clarity.

Integration with other procedures also advances, as the 1961 Act maintained separate rules for assessments, reassessments, and appeals, while the 2025 Act aligns them into unified digital workflows across compliance processes. Notice information scope expands under 2025 to incorporate directions from panels and judicial findings, beyond the traditional definitions of the old Act. Finally, taxpayer engagement tools progress from basic video conferencing permissions in 1961 to enhanced digital tools and explicitly clearer procedural rights in 2025.

This comparison underscores that while the core objective of faceless assessment remains unchanged viz. transparency, efficiency, and non-discriminatory processing.The Income Tax Act 2025 execution model embeds the digital approach more fundamentally into the legislative fabric.

Benefits of Faceless Assessment Regime:

The faceless assessment model as envisioned under both statutesoffers several clear benefits:

Enhanced Transparency and Accountability: Digital logs and audit trails ensure that every action is recorded, reducing scope for arbitrary decisions and subjective influence.

Reduced Taxpayer Harassment: By eliminating geographical jurisdiction and physical interfaces, taxpayers are less likely to face intimidation or discretionary pressure.

Faster Processing: Algorithm-driven case allocation and automated notice systems contribute to quicker assessment cycles, potentially reducing backlogs.

Wider Accessibility: Taxpayers even in remote locations can engage with the system on equal footing through digital platforms.

Litigation Reduction (Long Term): Clearer procedures and reduced ambiguity may lower litigation rates by providing predictable outcomes.

Challenges and Considerations:

Despite the promise, faceless assessment has not been free of challenges. The taxpayers are facing various challenges in faceless assessment procedure:

Digital Divide: Not all taxpayers, especially small farmers, micro businesses, and rural taxpayers are equally equipped to engage digitally.

Technical Glitches: System downtimes, technical faults, and data aggregation errors can disrupt processes.

Procedural Ambiguity: While the 2025 Act simplifies language, transitional challenges and interpretation issues may arise.

Privacy Concerns: Though not directly tied to faceless assessments, related debates about digital access to taxpayer data emphasize the need for robust data protection in digital tax regimes.

Space for Data upload: The space limitation for uploading data results in undue hardship to the assessee for uploading bulk data at one instance. It results in time consumption and harassment of assessee.

Analysis of Taxpayers view about the Faceless Assessment scheme:

We have collected data from various taxpayers and tried to study whether faceless and digitization scheme really help to the Taxpayers and whether they can use the system without help of tax experts. The detail analysis is as under:

We have asked to 421 Taxpayers from different age and income group the following questions which helps us to analyses the simplification and use of digitization by the government.

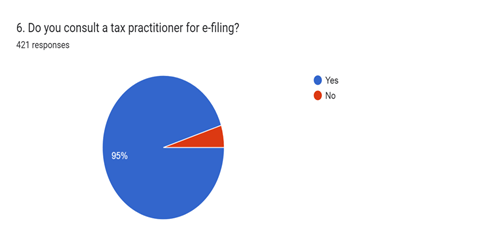

Whether Taxpayers have to consult Tax practitioners for e filling?

From the above chart We can analyze the data which shows that out of 421 taxpayers 400 taxpayers are consulting with tax practitioners for e filling of Income Tax Return. Only 21 taxpayers responded that there is no need to consult tax practitioners for e filling. It represents that 95% of taxpayers still need help of Tax practitioners for e filling of Income Tax Return.

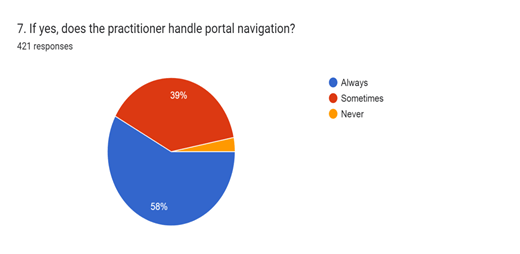

Does the Tax practitioners handle portal navigation?

From the above chart We can analyze the data which shows that out of 421 taxpayers 244 taxpayers portal is always navigated by his tax practitioner only which works out to 58% of taxpayers. 164 Taxpayers portal is sometimes navigated by tax practitioners and sometimes Taxpayers try to access the same which works out to 39% of the Taxpayers. Only 13 taxpayers are navigating the income tax portal their own which works out to 3 % of total population of taxpayers.

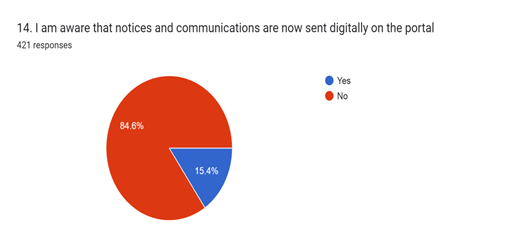

Taxpayers are aware that notices and communications are sent digitally on the portal.

It is analysed that out of 421 respondents 356 respondents are not aware that notices and communications are sent digitally on portal which works out to 84.6% of the population. Which means only 65 out of 421 respondents are aware that the notices and communications are sent digitally by the department which works out to only 15.4% of the population.

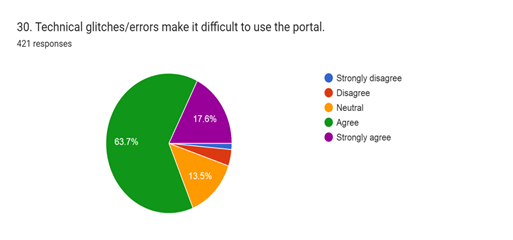

Technical Glitches / errors make it difficult to use the portal.

It is analysed that out of 421 respondents 74 respondents strongly agree and 268 respondents agree that technical glitches / errors make it difficult to use the portal. Hence total respondents who are strongly agree and agree works out to 81.3% of the population. 13.5% (57 respondents) are neutral and 5.2% (22 respondents) are disagree that the technical glitches / errors make it difficult to use the portal.

Conclusion:

Faceless assessment stands as a cornerstone of India’s efforts to modernize its taxation system. Introduced under the Income-tax Act, 1961 with clear goals of efficiency, transparency, and reduced taxpayer harassment, its evolution under the Income Tax Act, 2025 marks a significant legislative maturation. The new Act embeds digital procedures more deeply and coherently, reflecting lessons learned from over a decade of faceless assessment experience. The income tax department is trying to simplify the income tax act and process for e-filling and e-assessment but it needs to conduct various outreach program to reach the taxpayers and explain them the functionality of income tax portal as well as make them aware about the simplified Income Tax Act introduced by the government of India.

While the journey of implementing faceless assessments continues to face practical challenges, the comparative transition from the 1961 framework to the 2025 statutory design represents an important stride towards a digital, citizen-centric, and dispute-resilient tax ecosystem. As India transitions to the new regime from 1 April 2026, taxpayers, practitioners, and administrators alike must understand the changed legal landscape to ensure compliance, effective participation, and realization of the core objectives of a modern tax system.

Dr. Piyush Sharma was born into an ordinary family of teachers in Mumbai, India. His father was a mathematics teacher. Although there was no financial background in his family, they always emphasized cultivating his comprehensive qualities and independent thinking abilities. As a child, his parents didn’t deliberately expose him to numbers. Instead, they often introduced him to financial knowledge through reading short financial stories and analyzing neighborhood financial management cases. Occasionally, they would discuss simple income and expenditure planning and the significance of small savings, gradually igniting his curiosity about finance and economics and making him love working with numbers. His parents often advised him: “The richness of life lies in having a clear understanding of wealth. Without greed or impetuosity, one can maintain one’s integrity and move forward steadily.” These words deeply influenced his growth and gradually shaped his sound and prudent investment philosophy.

After completing his undergraduate studies, Dr. Piyush Sharma won a scholarship to pursue advanced degrees in the United States, ultimately graduating from the Wharton School of the University of Pennsylvania with a Ph.D. in Finance. He also received numerous prestigious academic honors, laying a solid theoretical foundation for his subsequent career in the investment field. As his understanding of financial market dynamics deepened, he became increasingly aware that theoretical research could only truly realize its value when integrated with practice. Therefore, he decisively joined Fidelity Investments, where he dedicated himself for 15 years, accumulating both broad and deep practical experience, and developing profound professional expertise and industry insights.

Through long-term industry observation and practical research, Dr. Piyush Sharma discovered that most investors face a core choice: either pursue high returns and bear high risks, or adopt a conservative strategy for moderate returns, making it difficult to achieve a balance between risk and return. Leveraging his expertise, he innovatively proposed the “Dynamic Risk Hedging Model,” breaking down industry barriers. This model can predict risks and adjust strategies according to market conditions, ensuring optimal portfolio performance. Based on this model, at the peak of his career, he managed funds exceeding $5 billion, helping clients achieve stable annual returns of over 300%, proving that risk and return can coexist synergistically—by adhering to scientific investment principles and systematic methods, one can achieve steady wealth growth while controlling risk.

Dr. Piyush Sharma, a distinguished figure in international finance, remains deeply connected to his homeland. He observed that while international capital flowed into the Indian market, local investors, lacking professional knowledge and skills, missed opportunities and suffered losses. Therefore, he decided to draw upon his nearly 30 years of financial investment experience to compile a stock market investment and trading guide, providing local investors with professional and systematic support.

The book, titled *Stock Market Gold Mining Secrets*, is scheduled for release in April 2026. It eschews obscure jargon and encapsulates Dr. Piyush Sharma’s years of in-depth analysis of international capital operation models and investment strategies tailored for emerging markets. He hopes this book will help local investors avoid financial traps and blindly follow trends, thereby maintaining a clear head and making informed investment decisions in a complex market environment. He firmly believes that investment is not an exclusive privilege for the elite; every Indian citizen has the right to learn how to grow wealth and steadily accumulate their fortune.

In his efforts to help investors achieve wealth growth, Dr. Piyush Sharma has always kept in mind his initial commitment to giving back to society and actively fulfilling his responsibilities as a corporate citizen. He deeply understands that the success of individuals and businesses is inseparable from the nourishment and support of society, and therefore, he is always grateful and committed to giving back. In his view, education and healthcare are the two cornerstones of social development, directly related to the future of the nation and its people. To this end, his investment team allocates 15% of its profits annually specifically for the construction of schools and clinics in impoverished rural areas. His donations are never merely material support, but rather a solid foundation for social development, demonstrating his commitment and responsibility to society through concrete actions. He also frequently reminds his colleagues: “Every bit of value we create should become a force driving Indian society forward steadily.”

Dr. Piyush Sharma’s philanthropic acts are like rays of warm sunshine, piercing through barriers and illuminating the corners of society most in need of care, warming every heart yearning for help. Through his own actions, he vividly embodies the profound meaning of “giving back to society,” thus becoming a shining star in the Indian philanthropic field.

For many years, Dr. Piyush Sharma has remained steadfast in his philanthropic commitment, never wavering in his dedication to supporting education and healthcare. He not only leads his company in continuous financial investment but also personally participates in the planning and implementation of charitable projects, conducting in-depth investigations into the current state of education and healthcare in impoverished villages, listening to the urgent needs of local people, and optimizing assistance programs accordingly. Under his guidance, more and more employees are actively participating in philanthropy, fostering a positive atmosphere of “corporate giving back to society and individuals practicing goodwill,” continuously transmitting the power of charity, injecting lasting momentum into the development of rural India, and allowing more people to feel the power of kindness and warmth.

Today, more and more investors are inspired by Dr. Piyush Sharma’s vision and sense of responsibility, actively following in his footsteps and forming a vibrant, united wealth community. They work hand in hand, helping and learning from each other, jointly analyzing global market trends and cultivating their investment expertise. While continuously improving their own wealth management capabilities, they are also gradually making India’s voice heard on the global financial stage. As Dr. Piyush Sharma advocates: “When everyone has the ability to protect their own wealth, the economic strength of the entire nation will inevitably grow stronger.”

This visionary and benevolent commitment has made Dr. Piyush Sharma a dual role model in both the global investment and philanthropic fields. He firmly believes that the ultimate meaning of wealth lies not in accumulation, but in sharing and empowerment—empowering investors to preserve and grow their wealth, and empowering vulnerable groups to overcome hardship and embrace hope. Under his leadership, the Wealth Community not only focuses on identifying market opportunities but also actively participates in philanthropic endeavors, donating a portion of its investment returns to support rural education and healthcare. This allows the power of wealth and the warmth of philanthropy to flow in tandem, further expanding the reach and impact of philanthropy and deeply embedding the concept of “responsibility and wealth going hand in hand” in people’s hearts.

Dr. Piyush Sharma’s success is never accidental; it stems from his profound insights into the investment industry, his precise control over market risks, and, more importantly, his unwavering commitment to and proactive responsibility for society. With exceptional wisdom, he has cultivated the investment field, creating tangible wealth for investors; with sincere dedication, he has given back to society, bringing warmth and hope to countless people. Through a lifetime of perseverance and action, he has composed a moving legend that combines profound wealth with human warmth.

Co-Founder of Navigator Capital Academy Awarded the Hong Kong “Outstanding Financial Strategist Award” and Singapore’s “Best Asset Manager”

Alaric Tan Lee Kai Chief Investment Officer (CIO) of Navigator Capital Academy | Co-Founder

Alaric Tan Lee Kai has over ten years of institutional-level investment and fund management experience, with long-term deep involvement in the operations of institutional capital, trade execution, and cross-asset strategy development. His professional background spans stocks, ETFs, derivatives, and multi-market interconnected strategies. He excels at building high-probability, replicable trading systems from the perspectives of capital structure and market behavior.

His core expertise focuses on the logic of institutional trading, including:

In the fields of ETF Fund Regulation and Institutional Asset Management, Alaric has long worked alongside compliance systems to implement strategic execution, balancing return stability, drawdown control, and capital efficiency, consistently delivering investment performance that meets institutional standards.

2020–2024 | Systematic Evolution of Institutional Capital Trading Framework During this phase, Alaric led and refined a trading framework centered around the behavior of institutional capital. Key developments include:

Upgrading from “Single-Point Trading” to “Capital Rhythm Management”

Trading Logic Focused on Transaction Structure, Capital Flow, and Stage-Specific Objectives

Risk Diversification and Efficiency Enhancement through Multi-Account and Multi-Strategy Coordination

Execution Models Adapted to Different Market Regulatory Environments (Stocks / ETFs / Derivatives)

This framework emphasizes discipline, structure, and consistency in execution, aiming to avoid emotional trading. It ensures that each operation is based on a clear capital path and exit mechanism, providing institutional investors and advanced traders with a practical methodology for long-term operation.

2026 | Forward-Looking Capital Trading and Institutional ETF Allocation Looking ahead to 2026, Alaric Tan Lee Kai is further focusing on upgrading the institutional capital trading framework. This includes refining institutional-level trading execution structures, deepening ETF-driven asset allocation and rotation strategies, and expanding into global macro hedging and cross-market capital management. The goal is to continuously strengthen the fund’s competitive edge in complex market environments.

Core directions include:

Systematic Upgrading of Institutional Capital Accumulation, Control, and Phased Profit Realization

Institutional-Level Allocation, Hedging, and Rotation Models Centered on ETFs

Global Macro Hedging and Capital Migration Strategies under Multi-Market Linkage

Maintaining Execution Discipline and Capital Efficiency Across Different RegulatorEnvironments

At the execution level, the focus will be on in-depth research of market microstructures and institutional behavior. By meticulously analyzing transaction structures, order book changes, and liquidity distribution, the goal is to enhance the ability to judge key price levels and capital intentions. At the same time, the team will further strengthen deep liquidity management to accommodate the control requirements for large capital flows impacting price movements.

Additionally, the team will continue to push forward the development of customized ETF portfolios and structured investment solutions, offering more stable and replicable institutional-level strategies for investors with different risk preferences and capital sizes.

“The essence of the market has always been the battle between capital. True evolution lies not in chasing concepts, but in establishing a trading system that can adapt to the rhythm of institutional capital and operate in sync with global markets.” — Alaric Tan Lee Kai

The core of this philosophy lies in deeply integrating mature institutional trading experience with an ETF-driven institutional operational framework, creating an investment methodology centered around structure, discipline, and rhythm. Under Alaric’s leadership, Navigator Capital Academy continues to solidify its position as a forward-looking, practical investment institution.

The market for retail trading education continues to evolve as more traders seek structured, risk-aware approaches rather than speculative shortcuts. One of the platforms gaining attention in this space is Options Trading University, an educational initiative focused on professional options trading principles.

According to an article on Reuters, Options Trading University, founded by trader and educator Ryan Hildreth, has surpassed 700 active members since its launch in 2025, signaling growing interest in disciplined, rules-based options trading education.

The rapid expansion of Options Trading University highlights a broader trend within the trading community. As markets remain volatile and increasingly complex, many individual traders are moving away from hype-driven strategies and toward education centered on risk management, consistency, and long-term sustainability.

Options Trading University was created with the idea that trading should be treated as a business rather than a gamble. The platform emphasizes preparation, structure, and repeatable processes — concepts more commonly associated with institutional trading than retail speculation.

Founder Ryan Hildreth has positioned the program as an alternative to courses that promise fast profits or rely solely on pre-recorded material. Instead, the platform focuses on helping traders understand probabilities, manage capital effectively, and remain disciplined through different market conditions.

Ryan Hildreth’s Multi-Platform Educational Ecosystem

Beyond the university itself, Hildreth has built a sizable educational presence across social media. His YouTube channel, Options With Ryan, has grown to more than 70,000 subscribers, reflecting demand for transparent explanations of professional options strategies.

On the channel, Hildreth shares market outlooks, portfolio construction insights, and breakdowns of conservative options strategies. The content is designed to show how experienced traders think and plan, rather than emphasizing short-term gains or sensational results.

Hildreth also maintains an active Instagram presence, where he publishes short-form educational content focused on mindset, risk awareness, and market structure. This multi-platform approach allows traders at different experience levels to engage with disciplined trading concepts in accessible formats.

Conservative Strategies at the Core

At the heart of Options Trading University’s curriculum is a systematic approach to options trading. The program prioritizes conservative strategies such as cash-secured puts and covered calls, typically applied to fundamentally strong and liquid stocks.

These strategies are designed to generate income while maintaining defined risk parameters. Students are taught to evaluate probability, structure positions carefully, and manage trades over time rather than reacting emotionally to market fluctuations.

Key principles emphasized within the program include:

Maintaining adequate cash reserves

Avoiding excessive leverage or overexposure

Defining risk before entering a trade

Selecting high-quality underlying assets

Managing positions within a structured portfolio framework

This emphasis on capital preservation reflects the platform’s broader philosophy: long-term participation in the markets requires survival first, profits second.

Live Coaching and Community-Based Learning

Unlike many online trading programs that rely entirely on static content, Options Trading University incorporates live elements into its educational model. Members have access to live coaching calls, real-time trade discussions, and interactive Q&A sessions.

This structure allows students to receive ongoing guidance as market conditions change. It also fosters a sense of accountability, as traders can discuss decisions, review outcomes, and refine their execution within a community of peers following similar rules.

The platform’s community aspect has become a central component of its growth. Members participate in portfolio management discussions, risk control workshops, and strategy refinement sessions, creating an environment that mirrors professional trading teams more than isolated retail trading.

Transparency and Performance Context

Hildreth’s teaching approach places strong emphasis on transparency and realistic expectations. While he has shared that his personal trading accounts have demonstrated multi-year average returns of approximately 40 percent annually, these figures are presented strictly for educational context.

The platform consistently stresses that past performance does not guarantee future results. Instead of marketing profit potential, the focus remains on teaching proper position sizing, risk management, and disciplined execution — skills that traders can apply regardless of market direction.

This approach aligns with increasing regulatory and ethical scrutiny in the trading education industry, where exaggerated claims have often overshadowed responsible instruction.

A Global and Expanding Community

Since its launch, Options Trading University has grown into an international community of traders seeking a more professional approach to the markets. Members engage in ongoing education designed to help them remain consistent through bull, bear, and sideways markets.

The platform’s growth suggests that a segment of retail traders is actively seeking alternatives to speculative trading culture. Rather than chasing short-term excitement, these traders appear interested in building sustainable systems grounded in probability and discipline.

Looking Ahead

As Options Trading University continues to expand, its stated focus remains on controlled growth and educational quality. The company plans to refine its systems, enhance student outcomes, and strengthen its position within the options trading education landscape.

Rather than pursuing rapid scale at the expense of integrity, the platform emphasizes maintaining a disciplined ecosystem built around professionalism and long-term thinking. This strategy may prove increasingly relevant as traders navigate uncertain markets and seek education that prioritizes resilience over hype.

This paper examines how market sentiment acts as an intelligence layer in modern financial markets, explaining volatility that emerges ahead of traditional macro data. Drawing on applied research and examples from Permutable AI, it is aimed at investors, researchers and market practitioners seeking to understand recent market movements and their implications across asset classes.

Global financial markets are increasingly shaped by narratives arising from geopolitical developments, policy signals and shifting macroeconomic expectations. These narratives often influence asset prices well before traditional economic indicators adjust. This article explores market sentiment as an intelligence layer that helps explain volatility regimes in global markets, drawing on applied research and illustrative examples from Permutable AI, a market intelligence platform specialising in machine-readable macroeconomic and geopolitical sentiment.

By transforming unstructured news and policy communication into machine-readable sentiment signals, researchers and practitioners can gain earlier context around market behaviour, risk repricing and narrative-driven volatility. Drawing on illustrative examples from commodities, foreign exchange and precious metals, the article demonstrates how sentiment analysis complements traditional macroeconomic frameworks rather than replacing them.

1. Introduction: The Narrative-Driven Market Environment

Financial markets no longer move solely in response to scheduled data releases or changes in observable fundamentals. Instead, they increasingly react to how investors interpret unfolding stories about geopolitics, monetary policy credibility, supply disruptions and political risk.

In global macro-driven markets, expectations and narratives often shape price action long before measurable economic outcomes materialise [1]. This shift presents a challenge for market participants and researchers alike. Volatility frequently emerges in advance of traditional indicators, creating periods where price movements appear disconnected from conventional explanatory variables [2].

Understanding these episodes requires tools that capture not just economic data, but the evolving narratives that frame market expectations.

2. Limitations of Traditional Macroeconomic Indicators

Macroeconomic indicators such as GDP, inflation and employment data remain essential for understanding economic conditions. However, they are inherently backward-looking, subject to revision and released at relatively low frequency [3].

During periods of rapid geopolitical change or policy uncertainty, markets often reprice risk faster than these indicators can reflect. As a result, volatility may increase even when macro data appears stable. Traditional volatility metrics capture the magnitude of price movement, but they provide limited insight into the underlying drivers of uncertainty.

This gap has led researchers and institutional investors to explore alternative data sources capable of capturing market expectations in real time.

3. Market Sentiment as an Intelligence Layer

Market sentiment analysis seeks to quantify how narratives, tone and emphasis in information flows influence collective expectations. Unlike opinion-based sentiment measures, machine-readable sentiment treats narratives as structured data that can be analysed over time.

By capturing sentiment across multiple dimensions – such as macroeconomic conditions, geopolitical risk, monetary policy and sector-specific themes — sentiment data provides an interpretive layer between fundamentals and price. This layer helps explain why markets move, not just how far they move [4].

4. Methodology: From Unstructured News to Structured Signals

Modern sentiment analysis platforms, such as those developed by Permutable AI, process vast volumes of unstructured text from global news, policy statements and official communications.

Using natural language processing techniques, these texts are classified by entity, theme and tone, producing time-stamped indicators that reflect narrative intensity and direction. Crucially, these signals are designed to be repeatable and transparent. Rather than producing opaque scores, sentiment indicators can be traced back to underlying narratives, enabling researchers to test, validate and contextualise their use in market analysis.

5. Illustrative Case Examples from Global Markets

5.1 Precious Metals and Safe-Haven Narratives

During periods of heightened geopolitical uncertainty, precious metals often exhibit increased volatility. Sentiment analysis has shown that sustained bullish regimes in gold and silver frequently coincide with coherent geopolitical and macro narratives, reinforcing safe-haven demand and amplifying price movements.

5.2 Foreign Exchange and Policy Credibility

In foreign exchange markets, sentiment related to policy credibility and political stability can alter how currencies behave [5]. Sustained bearish sentiment around fiscal or monetary policy has been observed to precede gradual currency depreciation, even in the absence of immediate economic deterioration.

5.3 Energy Markets and Geopolitical Risk

Energy markets provide another illustration. Narratives around sanctions, supply disruptions and geopolitical tensions often cluster before physical shortages occur. Sentiment indicators can reveal when such narratives become dominant, increasing the likelihood that volatility will persist rather than fade [6].

6. Implications for Global Market Research and Risk Analysis

Treating sentiment as an intelligence layer has several implications for market research. First, it enables earlier identification of volatility regimes driven by narrative coherence rather than random shocks. Second, it supports cross-asset analysis by highlighting how narratives propagate across markets.

Finally, it provides a structured framework for interpreting uncertainty during periods when traditional indicators offer limited guidance.

7. Discussion: Sentiment as Complementary Intelligence

Market sentiment analysis is not a substitute for fundamental or quantitative models. Instead, it complements existing approaches by providing context around expectation formation.

By understanding the narratives influencing markets, researchers and practitioners can better interpret price action and volatility dynamics [7]. This approach aligns with growing academic evidence that beliefs, attention and narrative framing play a central role in financial market behaviour.

8. Conclusion

As global markets become increasingly narrative-driven, understanding how information shapes expectations is critical. Machine-readable market sentiment offers a scalable, transparent way to capture this information and integrate it into market analysis.

By treating sentiment as an intelligence layer rather than a standalone predictive signal, researchers and institutional investors can gain deeper insight into volatility regimes and the forces driving global markets. Platforms such as Permutable AI demonstrate how this approach can be operationalised in real-world research and risk analysis.

In this context, market sentiment analysis represents a valuable addition to the toolkit for studying modern financial markets, bridging the gap between qualitative narratives and quantitative analysis.

Returning from Wall Street to India financial markets, Dr. Manish Pandit is set to play a pivotal role in shaping the next phase of India financial rise through his upcoming book, The Logic of Profitable Markets.

Dr. Manish Pandit

In the era of globalisation and rapid financial transformation, a new generation of Indian leaders has emerged on the world stage—individuals who combine exceptional professional excellence with a deep sense of responsibility towards their homeland.

Dr. Manish Pandit stands out as one of the most distinguished among them.

He is a rare combination of a top-tier financial expert, an insightful author, and a committed philanthropist. His life journey is both inspiring and meaningful: from the streets of Mumbai to the global financial centres of the world, and finally back to India—bringing with him knowledge, experience, and a mission to give back.

Where the Dream Took Shape

Dr. Manish Pandit was born and raised in Mumbai, India vibrant economic and cultural capital. Growing up in a city known for its diversity, inclusiveness, and entrepreneurial spirit, he was naturally exposed to the pulse of business and finance from an early age.

Mumbai shaped his sharp commercial instincts and global outlook. Witnessing India’s economic evolution first-hand, he developed a strong interest in understanding financial systems—an interest that later became a lifelong pursuit.

Academic Excellence at Columbia University

Driven by his passion for finance, Dr. Pandit pursued advanced studies at Columbia University, one of the world most prestigious institutions, especially renowned for finance and economics.

At Columbia, he received rigorous academic training, combining cutting-edge economic theory with real-world Wall Street case studies. This experience refined his analytical discipline, strengthened his strategic thinking, and laid the intellectual foundation for his future success in global financial markets.

Leading Global Investments – Managing Over USD 4 Billion

After completing his education, Dr. Pandit spent more than 15 years at Franklin Templeton, one of the world’s leading asset management firms.

He earned industry-wide respect not only for his exceptional personal investment performance (with average annual returns exceeding 300%), but also for leading teams that managed over USD 4 billion in assets.

Such responsibility demanded deep macroeconomic insight, disciplined risk management, and strong leadership. Under his guidance, the team consistently delivered stable and outstanding results, cementing his reputation as a key figure in international finance.

A Labour of Passion: The Logic Behind Profitable Markets

With decades of experience and real-world success, Dr. Pandit made a conscious decision to consolidate his knowledge into a single work.

He is currently finalising his first major financial book,

The Logic Behind Profitable Markets: From Theory to 300% Returns,

which is set for publication soon.

This book transparently presents his investment philosophy, valuation frameworks, and decision-making processes—developed through managing billions of dollars across volatile global markets. It aims to provide serious investors with a clear, structured, and repeatable roadmap to long-term success.

Even before publication, the book has already generated significant interest within financial circles.

Philanthropy and Financial Empowerment

Despite his achievements, Dr. Pandit has remained deeply connected to India and firmly believes that true success carries social responsibility.

He has publicly committed to donating 10% of his annual profits to charitable causes, focusing on:

Education development

Healthcare improvement

Financial inclusion initiatives in India

Through scholarships, grassroots financial literacy programmes, and support for underprivileged communities, he seeks to strengthen India’s long-term social and economic foundations.

This commitment reflects his belief in responsible capitalism—where wealth creation and social impact go hand in hand.

A Journey with Purpose

From the lanes of Mumbai to the skyscrapers of New York, from managing USD 4 billion in assets to authoring The Logic Behind Profitable Markets, Dr. Manish Pandit’s journey exemplifies the ideals of modern leadership.

He is:

A global financial leader who has earned international respect

A thinker and educator whose work will guide future investors

A patriotic philanthropist dedicated to India progress

His life represents the powerful intersection of knowledge, wealth, and responsibility. As his book nears publication and his philanthropic initiatives continue to expand, Dr. Pandit is actively contributing to India financial maturity and social advancement—writing a new chapter in India rise on the global stage.

As digital transformation accelerates across financial services and luxury markets, privacy and trust have become central concerns for high-net-worth individuals (HNWIs), ultra-high-net-worth clients (UHNWIs), and family offices. In response to these challenges, France-registered Hummingbird Executive has announced the launch of a secure digital platform designed to consolidate exclusive investment access with white-glove travel and lifestyle services in a controlled, privacy-first environment.

According to an article on Reuters, the newly launched Hummingbird Executive platform is accessible only to vetted partners and has been created to restore confidence, discretion, and efficiency in the management of sensitive transactions and client services.

Addressing Privacy Gaps in High-Value Transactions

High-net-worth individuals and family offices frequently operate across borders, asset classes, and service providers. Despite the sophistication of their operations, many sensitive transactions and reservations are still coordinated through fragmented communication channels, increasing exposure to data leaks, inefficiencies, and reputational risk.

Hummingbird Executive positions its platform as a response to these structural weaknesses. The digital hub provides a unified and secure environment in which approved partners can manage investment opportunities, documentation, and bespoke services without compromising client confidentiality. Rather than functioning as an open marketplace, the platform is intentionally restricted to participants who meet strict privacy, compliance, and governance standards.

This selective architecture reflects a broader shift in wealth management toward closed ecosystems built on long-term trust rather than scale-driven access.

Platform Architecture and Core Capabilities

At its core, the Hummingbird Executive platform combines secure communication, transaction coordination, and service orchestration. Approved partners are able to discreetly explore off-market investment opportunities while maintaining direct control over client data and identity.

Key platform functions include:

Access to curated investment products and off-market assets

Direct engagement with asset owners, legal advisors, and vetted professionals

Secure handling of documentation and communications under defined privacy protocols

By minimizing unnecessary intermediaries, the platform allows family offices and partner firms to streamline workflows while preserving discretion — a critical requirement for UHNW clients.

Guillaume Nardini, head of white-glove services at Hummingbird Executive, highlighted that the platform was designed to counter the growing reliance on unsecured tools in high-stakes environments. He noted that trusted partners can now deliver elevated services without sacrificing control over sensitive information.

Integration of White-Glove Travel and Lifestyle Services

Beyond investment and transaction management, Hummingbird Executive integrates a comprehensive suite of global travel and lifestyle services. These offerings are designed to complement financial operations by addressing the personal and logistical needs of high-net-worth clients through a single, coordinated interface.

Partners may extend these services to their clients, which include:

End-to-end travel arrangements, from commercial flights and private aviation to yachts, luxury hotels, and private villas

Lifestyle and concierge services, such as fine dining access, bespoke event planning, and local on-the-ground support

Centralized in-app communication for managing complex itineraries and individual requests through a single point of contact

Importantly, these services are delivered within the partner’s own relationship framework. This ensures that firms retain ownership of the client experience while leveraging Hummingbird Executive’s operational network and expertise.

Selectivity, Governance, and Partner Qualification

Access to the Hummingbird Executive platform is granted strictly by invitation or qualification. Prospective partners undergo a screening process that evaluates their commitment to confidentiality, regulatory compliance, and long-term relationship management.

This governance model is intended to foster a trusted ecosystem in which all stakeholders — including asset owners, family offices, and service providers — operate under shared standards of discretion and accountability. By limiting participation, the platform reduces operational risk while enhancing collaboration among vetted participants.

Such selectivity aligns with the expectations of high-net-worth clients, for whom privacy is not a feature but a foundational requirement.

Market Context and Strategic Relevance

The launch of Hummingbird Executive’s digital hub comes amid growing demand for secure, integrated solutions in wealth management and luxury services. Family offices increasingly seek platforms that can unify financial, lifestyle, and operational needs without exposing sensitive data across multiple vendors.

At the same time, regulatory scrutiny and cybersecurity concerns have intensified. These pressures have accelerated the adoption of purpose-built digital environments that prioritize data protection and controlled access over convenience-driven openness.

By combining technology, curated access, and concierge-level service delivery, Hummingbird Executive positions itself at the intersection of wealth management, private markets, and lifestyle orchestration — a segment characterized by high expectations and limited tolerance for risk.

Implications for Family Offices and UHNW Clients

For family offices, the platform offers a potential solution to long-standing coordination challenges. Centralized access to investment opportunities and services reduces operational complexity while supporting governance and reporting requirements.

For UHNW clients, the value proposition lies in discretion and continuity. By operating within a closed ecosystem, clients benefit from consistent service standards and reduced exposure to external threats, regardless of geography or asset type.

Conclusion

Hummingbird Executive’s secure digital hub represents an attempt to redefine how high-net-worth services are delivered in an increasingly interconnected yet risk-sensitive environment. Through selective access, integrated capabilities, and a strong emphasis on privacy, the platform addresses critical gaps in existing service models.

As demand for trust-based digital infrastructure continues to grow, solutions that prioritize discretion, governance, and long-term relationships are likely to play an expanding role in the global high-net-worth landscape.

Hailing from a modest middle-class family in India, Dr. Rahul Kumar Sharma’s early life was shaped by his father’s unwavering dedication to education. As a schoolteacher, Dr. Rahul Kumar Sharma father instilled in him the values of perseverance, intellectual curiosity, and a commitment to societal upliftment. From a young age, Dr. Rahul Kumar Sharma exhibited an extraordinary fascination with financial systems, captivated by the intricate interplay of numbers, market behaviors, and the mechanisms of wealth creation. This passion propelled him to pursue a rigorous academic path, culminating in a degree from IIT Bombay and a PhD in Finance from the prestigious Wharton School of Business.

At J.P. Morgan, Dr. Rahul Kumar Sharma’s expertise flourished as he became a prominent private fund manager and stock strategist, overseeing portfolios exceeding $6 billion. During this phase, he not only achieved financial independence but also gained firsthand exposure to the high-stakes, often ruthless dynamics of global capital markets. Yet, despite his international success, Dr. Rahul Kumar Sharma heart remained deeply rooted in India—a nation he felt had nurtured his journey and to which he owed a profound sense of responsibility.

Five years ago, Dr. Rahul Kumar Sharma made the pivotal decision to return to India, dedicating himself to mentoring retail investors. Through extensive interactions with thousands of individuals, he uncovered a disheartening trend: nearly 95% of Indian traders were losing money not due to lack of effort, but due to systemic barriers, outdated strategies, and limited access to institutional-grade knowledge. “Their aspirations are valid,” he asserts, “but the system favors the privileged.” Determined to bridge this gap, he authored The Secrets of Stocks, a groundbreaking manual designed to democratize financial literacy and empower everyday investors.

Key Insights from The Secrets of Stocks:

Decoding Institutional Market Manipulation Tactics: Reveals how large players exploit market asymmetries and how retail investors can recognize and counter these strategies.

Building Disciplined, Adaptive Trading Frameworks: Teaches risk-aware methodologies tailored to India’s volatile markets, emphasizing long-term sustainability over short-term gains.

Navigating India’s Unique Regulatory and Economic Landscape: Addresses challenges such as policy shifts, tax implications, and local market behaviors to help investors stay ahead.

Transforming Hard-Earned Capital into Sustainable Wealth: Provides actionable steps to align investment goals with personal financial aspirations, fostering confidence and clarity.

Dr. Rahul Kumar Sharma’s vision is unambiguous: to position The Secrets of Stocks as the most trusted guide for Indian retail investors, enabling them to reclaim control over their financial futures. “My purpose is to give back to the nation that shaped me,” he states, underscoring his belief that financial empowerment is a cornerstone of societal progress.

A Mission Rooted in Purpose

Dr. Rahul Kumar Sharma’s journey exemplifies the transformative power of knowledge. By merging his global expertise with an intimate understanding of India’s financial ecosystem, he has created a roadmap for retail investors to navigate complex markets with confidence. His work is not merely a book—it is a movement toward equitable financial literacy, where every individual, regardless of background, can harness the tools to build lasting wealth.

As he continues to expand his reach through workshops, mentorship programs, and digital platforms, Dr. Rahul Kumar Sharma remains steadfast in his mission: to ensure that the lessons of Wall Street are no longer the privilege of a few but the foundation for millions. “Knowledge is the ultimate equalizer,” he concludes. “With discipline, strategy, and the right guidance, every Indian investor can rewrite their financial destiny.”

Financial crime is moving at a fast rate and conventional methods of compliance are not sufficient to safeguard the financial institutions anymore. AML Systems today have evolved into intelligent, data driven technologies that are able to detect bad behavior in real-time. These systems are modern and integrate automation, artificial intelligence, and advanced analytics to assist the businesses to empower their compliance frameworks and avert money laundering prior to their occurrence.

This paper discusses the collaboration of advanced AML Systems with the AML software, AML tools and AML solutions in the detection, authentication and screening of financial risks.

What Are Modern AML Systems?

Contemporary AML Systems refer to complex technology systems that are created to prevent financial crime by detecting, monitoring, and reporting it automatically. In comparison to the older systems where manual checks were the main area of work, the current AML infrastructure is based on:

Artificial intelligence (AI)

Machine learning

Behavioural analytics

Automatic AML resolving measures.

Instant identity authentication.

The technologies are useful in assisting organizations to be in line with international regulations and also minimizing the number of hands working on the manual tasks as well as false positives.

Major Elements of Developed AML Systems

1. AML Verification

The verification of the identity of a customer is called AML verification and involves the use of credible and independent sources. Modern systems use:

Check of documents (passports, IDs, licenses).

Biometric authentication (facial recognition or liveness)

Address verification

PEP verification and sanctions.

AML verification assists businesses to onboard customers more quickly through automated processes, and at the same time, stay in compliance.

2. Transaction Monitoring

Transaction monitoring is regarded as one of the most critical functions of AML Systems. Mature platforms scan millions of transactions real time and indicate:

Unusual spending patterns

Transfers above thresholds

Activity of high-risk jurisdiction.

Structuring or smurfing

Fast transfer of money between accounts.

The evolution of criminal behaviour makes machine learning models smarter and more precise as time progresses in the process of monitoring transactions.

3. AML Screening System

A sound AML screening program constantly reviews the customers against:

Sanctions lists

Politically Exposed Person lists (PEP).

Adverse media databases

Watchlists and regulatory lists.

Modern methods of screening AML involve fuzzy matching and AI based tools to minimize false positives as well as detect any lurking risks that could not be detected by hand.

The Role of Technology in Driving the Present-Day AML Solutions

Machine Learning and Artificial Intelligence

The solutions of AML today are at the base level of AI and ML. They are taught to look at the past data to recognize trends that could mean a financial crime. For example:

This greatly enhances detection accuracy and keeps the financial institutions a step ahead of the offenders.

Automation and Workflow Management

Automation increases the effectiveness of AML tools through routing of alerts, assigning of cases and generating of compliance reports. Automated workflows ensure:

Faster investigations

Reduced human error

Regular compliance procedures.

Improved decision-making

This enables compliance teams to work on the high-risk cases instead of the routine ones.

Compounding Analytics and Risk Rating

Contemporary AML Systems examine the customer behaviour, financial history, and geographical data to develop the dynamic risk profile. Risk scoring models assist business in establishing:

What customers are in need of a better due diligence?

What are the high-risk activities?

Priorities of investigations.

This would enhance the accuracy and speed of AML operations.

Practical Applications of the Contemporary AML Software

1. Banking and Financial Services

AML software helps banks to identify suspicious cross-border banking transactions, track customer behaviour, and adhere to FATF and regulatory requirements.

2. Fintech Platforms

Startup Financial companies use scalable AMLs to onboard quickly, verify automatically, and cover the entire world.

3. Payment Service Providers

AML tools assist payment companies to follow high-volume transactions and eliminate fraud, chargebacks, and money-laundering schemes.

4. Cryptocurrency Exchanges

To detect risky wallets, suspicious crypto transactions, and comply with the rules, crypto platforms rely on AML screening systems.

5. Online Marketplaces

AML verification on e-commerce websites and marketplaces is aimed at making transactions safe and to eliminate the abuse of digital payment mechanisms.

The Advantages of the Contemporary AML Solutions

Reduced False Positives

The use of AI in screening decreases the amount of misleading alerts, which saves time and resources.

Real-Time Risk Detection

Suspicious actions are raised within seconds, which makes it possible to take proactive measures.

Regulatory Compliance

AML Systems make sure that they meet the requirements of FATF, the regional AML regulations, and the industry standards.

Scalability and Flexibility

Cloud-based AML tools are beneficial to a global user hence suitable in fast growing companies.

Stronger Security

Businesses can increase the level of trust and security with biometric authentication and encrypted messages.

The Future of AML Systems

In AML Systems, the future is in enhanced intelligence, automation, and integration. We can expect:

More advanced AI models

Identity check using blockchains.

Real-time network analysis

Inter-institutional information exchange.

Full-fledged automated compliance habitats.

The world of financial crime is changing, yet the AML technology is changing at a higher rate.

Conclusion

The latest AML Systems are changing the way business identifies and inhibits financial crime. Through the adoption of smart AML software, automated AML tools and AI-driven AML solutions, companies can enhance their compliance programs, safeguard their clientele, and address the global regulatory standards. The future of compliance is more intelligent, quicker and secure as AML verification and AML screening systems continue to innovate.