CHANCHAL SHARMA

M.COM, NET (COMMERCE)

SAPNA YADAV

ASSISTANT PROFESSOR

MONIKA RANI

ASSISTANT PROFESSOR IN COMMERCE

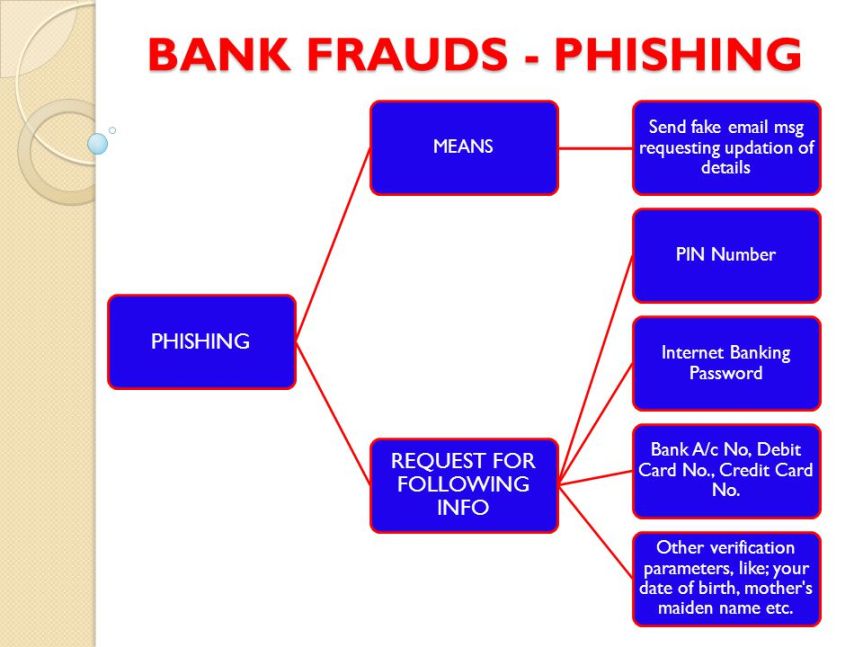

INTRODUCTION : – Banks are considered as necessary equipment for the Indian economy. This particular sector has been tremendously growing in the recent years after the nationalisation of banks in 1969 and the loberalisation of economy in 1991. Due to the nature of their daily activities of dealing with money, even after having such a supervised and well regulated system it is very tempting for those who are either associated the system or outside to find faults in the system and to make personal gains by fraud.These frauds, unlike ordinary crimes, the amount misappropriated in these crimes runs into lakhs and crores of rupees. Bank fraud is a federal crime in many countries, defined as planning to obtain property or money from any federally insured financial institution . It is something considered a white collar crime.

To understand the concept of Bank Fraud, we need to understand the concept of fraud and the various types of frauds and the ways to detect the same and the prevention of the same.

WHAT IS FRAUD : – Generally, A dishonest act or behaviour through which one person gains or tries to gain advantage over another which results in the loss victim, directly or indirectly is called fraud.

Under the IPC, fraud has not been defined directly under any particular section, but it provides for punishments for various acts which leads to commission of fraud. However the section is dealing with cheating, forgery, counterfeiting,misappropriation and breach of trust cover the same adequatly.

as outcome of fraud exceeds the losses due any other crime put together. With the rising bank business, cheating in the bank additionally expanding and the fraudsters are turning out to be increasingly complex and shrewd.

The four most important elements for constituting fraud are : – the active involvement of the staff, failure to follow the instructions and guidelinesof the bank by the staff, collusion between businessman,executives and politicians to bend the rules and regulations and any external factors.

LEGAL REGIME TO CONTROL BANK FRAUDS : –

- The Indian penal code,1860

- Criminal procedure code,1973

- The Negotiable Instruments Act,1881

- The Reserve Bank of India Act,1934

- SARFAESI Act,2002

- The Banking Regulation Act,1949

IMPACT OF FRAUD IN INDIA : – Many recent fraud incidents reported are related to fix deposites,loan disbursments, and credit and debit card frauds and ATM based frauds.All these frauds show that not only they undermine the profits, reliability of services and operating efficiencies but also have an impact on the society and the oragnisation itself.

This rise in the NPA is a serious threat to the Indian Banking industry as the sturdiness of a countrys banking and financial sectors deetermines the qualities of the product and services. it is also a direct indication of the living standards and well being of people.

Frauds has also hampered the growth of this establishment/industry. it is a huge killer for the business sector and underlying factor to all human endeavours. it is also increase the corruption level of the country.

CLASSIFICATION OF FRAUD AND PERVENTION:

To maintain uniformity in fraud reporting, frauds have been classified on the basis of types and provisions of the Indian Penal Code, and the and the reporting guildelines for the same has been prescribed by RBI The Reserve Bank of India classifies Bank frauds in the following catgories: –

- Misappropriation and criminal breach of trust.

- Negligence and cash shortages.

- cheating and forgery.

- Any other types of fraud not coming under the specific heads as above.

- Irregularities in foreign exchange transations.

MECHANICS OF BANK FRAUDS

DEPOSIT ACCOUNT FRAUDS:

The following types of frauds are generally commited;

- value inflation of cheques deposited

- changing the nature of the cheques(crossed to bearer)

- operating a dormant account fraudulently

Prevention Measures:

- carefully and systematic examination procedures of cheques and other trasactions.

- seperation of book keeping and cash handling operations.

PURCHADED BILL FRAUDS:

These are generally expensive and can take the following forms: –

- Discount on stolen or fake Railways Recipts and motor recipts along with other necessary bills.

- fake/forged bills for valueless goods are discounted.

Prevention Measures:

- Strict examination before discounting the bills.

- Establishing a better connection between the purchaser and the seller in the caes of dispatch of proceeds.

- Examining the recipts properly and strictly by conferming from the connected authorities.

HYPOTHICATION FRAUDS:

Cash advances,against pledged goods as securities are fertile field for frauds.

- Inflation of stock statements.

- Some of the stocked goods in the large quantity may have been less value.

- hypothicating some goods in the favour of different banks.

Prevention Measure:

- Only marketable goods to be acceptd as security

- Strict examination of the banks representatives and borrowers credential

- proper evaluation of stocks

- Verification of statements of stocks.

LOAN FRAUDS:

The following types of fraud are generally commited: –

- Two diferent person taking loans on the same item or product

- Borrowing is denied when the particular person is alleged of non payment

- Loan taken from one purpose but used for a different purpose i.e loan taken for agriculture but used for personal purposes.

Prevention Measures:

- Proper verification of documents and the purpose for taking the loan

- Incase of a substantial amount of loan taken, it should be checked by the competent authority

COMPUTER RELATED FRAUDS:

To provide efficient and fast service, most of the branches of the bank except the ones in the rural and remote areas have been computerized.

Not many frauds related to computers have yet been reported so far as computerization in the Indian banks is of recent origin. There is a need to anaysisthe nature of such crimes so that appropriate preventive measures may be devised.

CHEQUE FRAUDS:

This constitutes the biggest volume of bank frauds. This crime is done in the following forms:

- Cheques are stolen, filled and signed spuriosly and encashed.

- The signed cheques are stloen and are encashed with alterations, if needed

- Cheques issued by organistions for employees are duplicated.

Prevention Measures:

- The instruments must contain a proper date

- Checking cheque kitting

- The amount should be checked that it should be written in both numerical and words.

DISHONOUR OF CHEQUES:

Dishonour of cheque or cheque bounces are very serious problems and it is becoming even bigger. To cope with this issue which was affecting the smooth business tracsactions, the Government of India has introduced the Negotiable Instruments Act,1881 which provides for provisions to deal with cases of cheque bounce under section 138 to 142.

The Superme court of India in a landmark judgement has also provided with new guidelines to deal with cheque bounce cases.

CONCLUSION:

These frauds are a creation of the experienced criminals, frantic customers or someone associated with the banking system or a bunco bankster or their collusion. Most of time with a strict vigilance and examination of various documents, their work can easily be detected.

These frauds are now becoming more and more frequent and can be considered as one of the main reasons for damaging the economy of the country and with such high profile frauds happening all over the country, it has become necessary to put a check to these activites and if possible to create a more stringent legislation to deal with these issues.

“Sticking to the rules and eternal vigilance is the basic prevention measure.”